On a Monday morning in Atlanta, a bank COO can see the problem from three directions at once. Customers want faster digital service. Product teams want to launch new capabilities without waiting on a core release window. Operations teams are still spending too much time working around systems that were built for a different payments era.

That tension is where most modernization programs begin. Not with a dramatic boardroom mandate, but with a pile of practical constraints. A lending workflow that still depends on batch processing. A treasury platform that can't integrate cleanly with newer services. A data center footprint that keeps growing even as leadership talks about cloud migration.

The institutions getting this right aren't treating modernization as a narrow software project. They're treating it as a full lifecycle decision. That includes architecture, security, operations, compliance, vendor governance, and the final physical retirement of aging hardware. If you're evaluating how Atlanta banks are modernizing IT systems, that last part matters more than most leadership teams expect.

The Modernization Imperative for Atlanta's Financial Hub

In Atlanta, banks don't get the luxury of moving slowly just because their core systems are old. This is a major financial market with strong regional competition, a deep fintech presence, and customers who compare their bank experience with every polished digital service they use elsewhere.

A familiar pattern shows up in leadership meetings. One executive wants faster rollout of treasury features. Another wants cleaner reporting and fewer handoffs between departments. The CIO knows the true obstacle isn't a missing dashboard. It's that too many critical processes still depend on tightly coupled platforms, custom integrations, and infrastructure that's expensive to maintain.

What leaders are really deciding

The key decision usually isn't whether to modernize. It's how to modernize without breaking service, creating audit gaps, or turning a manageable transition into a multi-year disruption.

Most banks in this position are balancing competing realities:

- Customer pressure: Retail and commercial clients expect digital channels to work consistently, not just during ideal operating windows.

- Operational drag: Staff members compensate for system limitations with manual reconciliation, duplicate entry, and side spreadsheets.

- Risk concentration: The older the stack, the more institutional knowledge gets trapped in a few people and aging environments.

- Physical consequences: Every migration, platform consolidation, or branch technology refresh leaves behind retired servers, storage arrays, laptops, and network equipment that still carry risk.

Old infrastructure rarely fails all at once. It creates friction first, then delay, then risk.

That's why the strongest modernization programs in Atlanta don't stop at cloud strategy or API planning. They map the entire technology lifecycle from current-state assessment to decommissioning. Once a bank starts moving workloads, replacing edge hardware, shrinking on-prem footprints, or redesigning customer journeys, it also creates a growing stream of retired assets that need documented handling.

Leadership teams that ignore that final step usually discover the problem late. Hardware sits in staging rooms. Drives wait for destruction approval. Facilities teams and IT teams each assume the other owns the process. That's how an otherwise solid modernization effort turns messy.

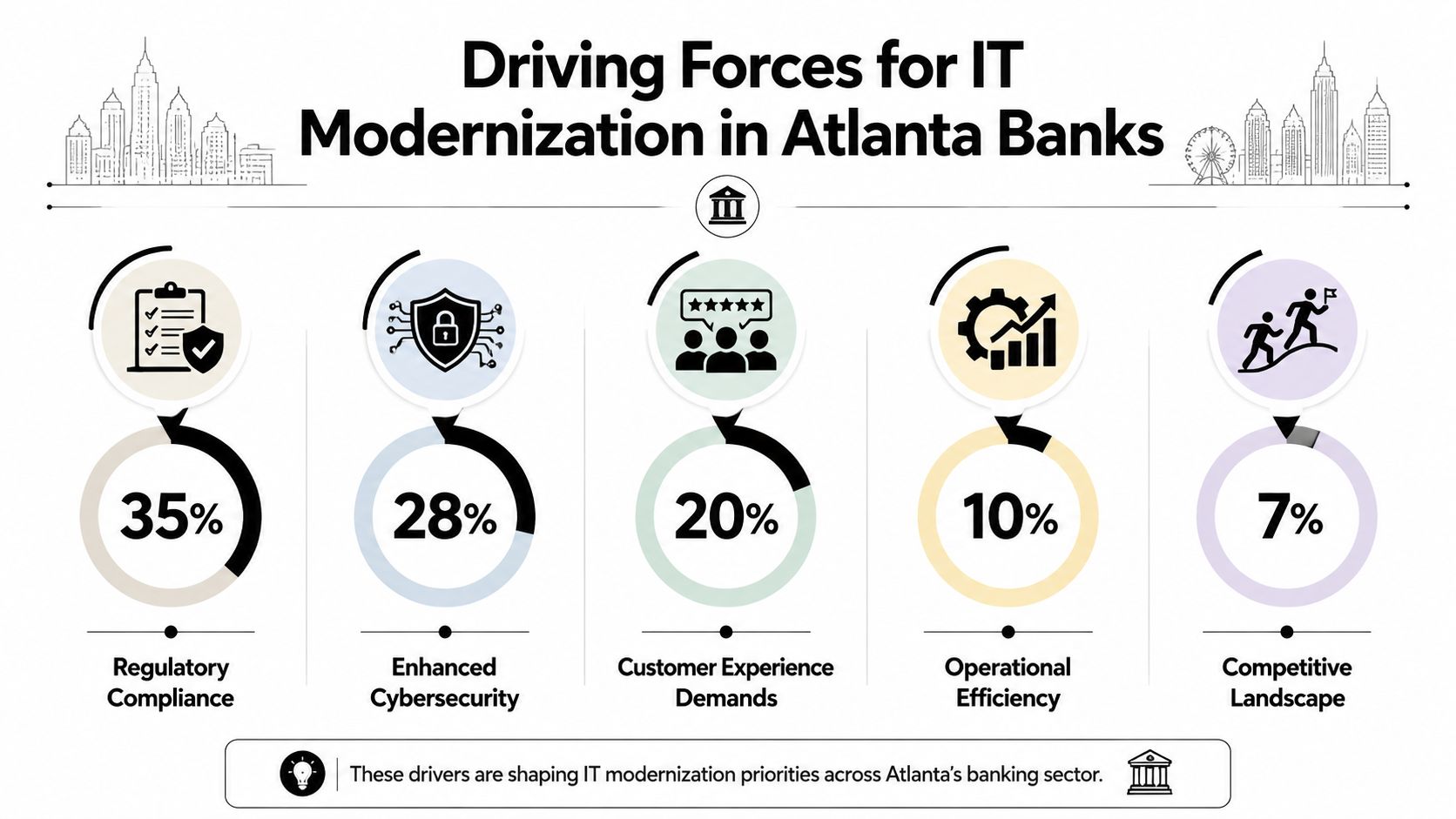

The Driving Forces Behind Banking IT Modernization

Atlanta banks are modernizing because the cost of standing still has become too high. This isn't just about keeping up with digital trends. It's about freeing budget, reducing operational strain, and making the institution easier to run.

One of the clearest signs is the burden of legacy technology itself. An industry estimate cited in a discussion of financial services modernization says 73% of financial institutions are still tied to legacy systems, and up to 70% of IT budgets can be consumed by maintaining outdated systems. That same discussion projects legacy platforms could cost the sector $57 billion by 2028 if not addressed (industry discussion of legacy payment modernization).

The pressures that actually move budgets

Banks rarely fund major IT change because a technology team asks for newer tools. They fund it when old systems interfere with revenue, service quality, or risk management.

Here's how that usually shows up in practice:

| Pressure | What leadership feels |

|---|---|

| Digital competition | Faster product launches from newer entrants and more responsive competitors |

| Customer expectations | Demand for smoother onboarding, self-service, and fewer service delays |

| Cost control | Too much spend trapped in maintenance, patches, and specialized support |

| Regulatory workload | Harder evidence gathering when systems are fragmented |

| Resilience needs | Greater pressure to reduce operational dependency on aging infrastructure |

Why legacy costs become strategic costs

A bank can tolerate old technology for years if the environment stays stable. Banking doesn't stay stable. Product mixes change. Payment expectations shift. Fraud controls evolve. Vendor ecosystems expand. Every one of those changes becomes harder when the bank's architecture was built around inflexible cores and point-to-point integration.

That's why I usually tell leadership teams to watch for three warning signs.

- Budget trapped in preservation: The institution spends heavily just to keep current systems operable.

- Slow delivery cycles: Product and operations teams wait on tightly coupled release calendars.

- Weak retirement discipline: Outdated hardware remains in circulation because nobody wants to touch the decommissioning workflow.

A lot of that third issue gets overlooked. Yet it often sits beside broader IT risk. Banks that are reviewing IT risk management trends for Atlanta businesses usually find that modernization and retirement controls belong in the same governance conversation.

Practical rule: If your architecture roadmap doesn't include a retirement roadmap, your modernization plan is incomplete.

Inaction has its own cost profile

Leadership teams sometimes frame modernization as disruptive and expensive. It can be. But maintaining aging systems is also disruptive and expensive, just in a less visible way. The costs get buried in exception handling, staff workarounds, elongated vendor projects, hardware maintenance, and delayed product delivery.

That's why the strongest business case for modernization usually isn't “new technology.” It's a simpler operating model with fewer constraints.

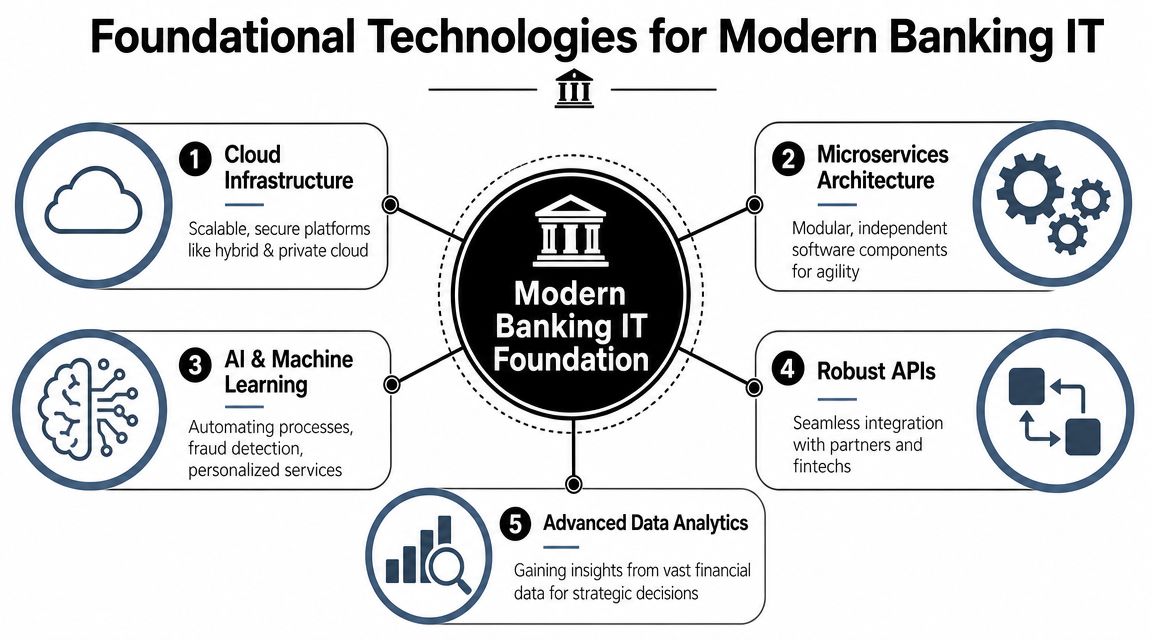

Key Architectures and Technologies Shaping the Future of Banking

Most successful banking modernization programs don't start with a full core replacement. They start by building an architecture that gives the bank room to move. The objective is simple. Reduce dependency on brittle connections, improve scalability, and make it easier to release change safely.

A major technical driver is support for instant payments and other low-latency services. Legacy cores often struggle here without architectural changes. The Kansas City Fed notes that next-generation core systems use modern architecture and plug-and-play features to support these services, while cloud migration is increasingly used to improve scalability and resilience. Related industry commentary also points to cloud-based technologies and API-forward architectures as ways to lower operational cost and increase scalability (Kansas City Fed research on core modernization options).

Cloud is an operating choice, not just a hosting choice

Executives often hear “cloud migration” and picture a location change. In practice, the bigger shift is operational. Cloud done well gives teams a better way to scale compute, improve resilience, standardize environments, and provision infrastructure without waiting on legacy procurement cycles.

For banks, that usually means a selective model. Not every workload should move at the same pace, and not every service belongs in the same environment.

A practical decision screen looks like this:

- Keep sensitive or tightly coupled workloads where they are until dependencies are mapped and controls are ready.

- Move variable or integration-heavy workloads first where elasticity and modernization benefits show up fastest.

- Standardize before migrating so the bank doesn't carry old complexity into a new platform.

APIs are what turn old capability into usable capability

An API-first approach matters because banks rarely get to rebuild everything from scratch. APIs let the institution expose useful legacy functions in a controlled, reusable way. That makes it easier to connect customer channels, internal applications, fintech partners, and reporting tools without custom one-off bridges every time.

When this is done poorly, the bank creates another layer of complexity. When it's done well, APIs become the contract between old and new systems.

A few design choices matter more than often anticipated:

- Govern the API catalog centrally

- Treat security controls as part of the product

- Design for reuse, not project-specific shortcuts

- Document dependencies before release

AI and analytics only work if the plumbing works

Banks don't get much value from AI or machine learning if the underlying data is fragmented, late, or hard to trust. The practical sequence is usually infrastructure first, integration second, data discipline third, then advanced use cases.

That includes fraud monitoring, operations support, document processing, and service personalization. But the primary enabler is a cleaner data foundation.

A lot of Atlanta institutions are also revisiting branch, edge, and distributed processing architecture as part of that effort. Broader edge computing trends in Atlanta businesses matter here because local compute, network resilience, and branch technology refreshes often intersect with banking modernization in very concrete ways.

The technology stack works best when leadership stops asking, “What tool should we buy?” and starts asking, “What operating capability are we trying to build?”

Navigating Security and Regulatory Compliance in the Modern Era

Some leadership teams still treat modernization as a temporary increase in risk. That can be true if the program is rushed, under-governed, or fragmented across too many vendors. But a disciplined modernization effort usually improves the bank's control environment.

Older environments tend to hide risk in places that are hard to audit. Permissions grow over time. Manual workarounds become normal. Data moves through systems without clear ownership. Logging is inconsistent. Reporting depends on tribal knowledge. That's not safer because it's familiar. It's just older.

Modernization can strengthen controls

Modern platforms give banks a chance to tighten identity controls, improve monitoring, segment workloads more cleanly, and build better evidence trails for exam and audit activity. That doesn't happen automatically. It happens when security architecture is part of the design, not a review step at the end.

A useful way to think about it is through the lens of a documented business compliance framework. Leadership needs a structure for who owns requirements, how controls are tested, where evidence lives, and how exceptions are escalated. Modernization gives the bank a chance to make those mechanics clearer.

The organizational gains matter too

A global survey of banks found that 70% reported improved collaboration after investing in fintech-enabled modernization, while 54% said digital transformation initiatives accelerated. The same research found 56% experienced market expansion, 55% acquired new customers, and 51% improved customer engagement, showing that modernization changes how the business operates, not just what technology it runs (global benchmark on bank modernization and fintech).

That matters for compliance because fragmented organizations usually produce fragmented control execution. When teams collaborate better, banks can manage change approvals, issue remediation, and control testing more consistently.

Security work that actually holds up

I advise banks to pressure-test modernization plans against a few simple questions:

- Can you prove data lineage across old and new systems?

- Can you demonstrate who approved each migration decision?

- Can you revoke access quickly across the full environment?

- Can you document what happened to retired hardware and stored media?

That last question tends to arrive late in the process. It shouldn't. Hardware retirement, storage handling, and disposition records should sit in the same governance stream as logical access and migration controls.

Banks reviewing obligations under state data breach laws usually realize that weak end-of-life handling can turn a routine infrastructure project into a reportable event. If retired drives, backup devices, or branch equipment leave controlled custody without documented destruction or sanitization, the technology project may be complete while the risk remains very much alive.

Compliance teams don't need modernization to be flashy. They need it to be provable.

The Final Mile Secure Legacy System Decommissioning and ITAD

During these phases, many programs lose discipline. A bank approves a phased migration, retires workloads gradually, shrinks part of a data center footprint, refreshes branch gear, and replaces end-user devices. Progress looks good on dashboards. Then the outgoing assets start piling up.

Banks usually modernize in phases rather than through a single rip-and-replace. Bain describes a common pattern as updating the distribution layer first, adding an API-based integration layer to the legacy core, and then rebuilding customer journeys over time. That approach reduces risk and creates a steady stream of decommissioned assets rather than one massive retirement event (Bain on phased bank technology modernization).

Why decommissioning needs its own workstream

A phased architecture changes the disposal problem. Instead of one large event at the end, the bank gets waves of retired equipment:

- branch servers

- SAN components

- tape media

- network appliances

- employee laptops

- test hardware

- racks, rails, PDUs, and supporting infrastructure

Each category has different handling needs. Some assets may be reused internally for a short period. Some may require secure data destruction before leaving custody. Others may be suitable for donation-based recycling or downstream materials recovery once chain-of-custody requirements are satisfied.

This isn't a facilities cleanup issue alone. It's a joint process across IT, information security, compliance, procurement, and facilities.

What good ITAD looks like in banking

For banks, IT asset disposition (ITAD) isn't just about hauling away old equipment. It's about proving what happened to each asset. That means serialized inventory, disposition decisions, custody records, sanitization or shredding workflows, and environmentally responsible downstream handling.

A workable decommissioning model usually includes:

| Step | What the bank should document |

|---|---|

| Asset identification | What equipment is being retired and who owns approval |

| Data handling decision | Wipe, shred, retain, or quarantine |

| Chain of custody | When the asset moved, by whom, and under what controls |

| Final disposition | Reuse, recycling, destruction, or donation pathway |

| Evidence retention | Certificates, logs, inventory updates, and audit support |

Retiring a server without retiring its risk is not completion. It's backlog.

This is also where a specialized partner can fit. Reworx Recycling provides services tied directly to this phase, including secure data destruction, electronics recycling, equipment decommissioning, pickups, and IT asset management support. For banks planning controlled retirement of aging infrastructure, a practical reference point is this server decommissioning checklist, which aligns the physical teardown process with risk and documentation needs.

The environmental and community side still matters

Financial institutions can't focus only on data risk. The environmental side matters too, especially when modernization generates large volumes of obsolete electronics. Responsible handling supports internal sustainability goals and keeps reusable equipment from being treated as generic waste.

Donation-based recycling also has a place in the lifecycle when policy, device condition, and data handling requirements allow it. A bank may not donate every retired asset. It can still build a disposition hierarchy that prioritizes reuse where appropriate and certified recycling where reuse isn't possible.

That's the full picture of how Atlanta banks are modernizing IT systems. Not just new cloud environments and cleaner APIs, but controlled retirement of the old estate.

Your Modernization and Disposal Checklist

A strong modernization plan should be executable by operations, security, compliance, and facilities teams without guesswork. If the program depends on institutional memory or informal handoffs, it won't hold up under pressure.

Use this checklist to tighten both the digital transformation work and the physical retirement work around it.

Start with control over the current state

Before any migration or refresh begins, get the inventory right.

- Map hardware and software together: Don't separate infrastructure inventory from application dependency mapping.

- Identify data-bearing assets early: Servers, laptops, backup media, branch devices, and storage appliances need explicit handling paths.

- Define business owners: Every critical platform should have an accountable owner outside the project office.

Set decision rules before assets move

Banks get into trouble when teams improvise disposition decisions after equipment is already disconnected.

- Write data eradication standards for different asset classes.

- Define chain-of-custody requirements for internal transfer, storage, pickup, and destruction.

- Separate reuse from recycling decisions so assets aren't mishandled in staging areas.

A practical planning aid is a formal compliance checklist template that lets teams align inventory, approvals, retention requirements, and disposition records in one workflow.

Build the vendor and governance layer

Not every provider belongs in a bank modernization program. Leadership should screen partners for documentation discipline, secure handling processes, and their ability to support audit requests after the project closes.

Look for these basics:

- Documented pickup and custody procedures

- Support for secure data destruction

- Clear reporting on final disposition

- Ability to coordinate office cleanout, facility cleanout, or data center decommissioning work

- Sustainable recycling pathways for non-reusable equipment

Make communication part of the project plan

Modernization affects more people than the infrastructure team. Relationship managers, branch operations, cybersecurity staff, legal teams, and facilities personnel all need clear expectations.

A clean technical cutover can still create operational confusion if the bank doesn't communicate what is changing, who owns each step, and when old equipment leaves controlled space.

That communication plan should answer basic questions. What is being retired. Where it will be held. Who authorizes release. What evidence gets retained. Who signs off when the retirement is complete.

Treat disposal as part of project closure

Many banks mark a project complete when the new platform is live. The better standard is stricter. A modernization initiative isn't closed until the old environment is either formally retained under policy or physically retired under documented controls.

That includes:

- Removing obsolete assets from inventories

- Confirming destruction or sanitization records

- Reconciling what was scheduled for retirement against what left

- Reviewing environmental handling outcomes

- Archiving evidence for future audit and legal review

If your bank is planning a branch refresh, infrastructure consolidation, office cleanout, laptop disposal cycle, secure data destruction workflow, or full ITAD program, start with the retirement process now, not at the end.

If your team is upgrading systems and needs a controlled way to retire outgoing hardware, Reworx Recycling can be part of that final-mile plan. Businesses can use the company's resources to evaluate secure data destruction, electronics recycling, IT equipment disposal, and pickup logistics as part of a broader modernization program. For Atlanta banks and other regulated organizations, the practical next step is to review current retired assets, identify what's sitting in storage or staging, and schedule a documented pickup or partner discussion before that backlog becomes a risk.