An auditor asks for proof that a batch of retired servers was securely destroyed years ago. The request sounds simple until someone has to locate the asset list, the chain of custody, the destruction record, the review signoff, and the reason a few drives were handled differently from the rest. That's when weak documentation stops being an administrative nuisance and becomes an operational problem.

Audit documentation requirements are relevant to people outside the audit department. IT leaders need records that prove what left the environment. Facilities teams need records that show where equipment went. Sustainability leaders need records that support responsible disposition decisions. If your company handles electronics recycling, computer recycling, secure data destruction, office cleanout projects, facility cleanout work, or data center decommissioning, auditors will expect a file that tells a coherent story without guesswork.

The problem usually isn't lack of effort. It's fragmentation. One record sits in a ticketing system. Another lives in a vendor portal. A spreadsheet tracks serial numbers, but no one preserved the review date. A destruction certificate exists, but it doesn't clearly tie back to the exact assets removed from service. Audit readiness fails in those gaps.

That pressure isn't unique to one country or one framework. Teams dealing with multinational operations often compare U.S. audit practices with broader governance expectations, and resources on mastering Australian compliance can be useful for understanding how documentation discipline carries across regulatory environments.

The Auditor Is Calling Your Guide to Being Prepared

An external auditor rarely starts with your internal constraints. They start with a request. Show the evidence. Identify the assets. Explain the exception. Confirm who approved the work.

That's why retired hardware creates such a revealing test. A laptop disposal event, a laboratory equipment disposal project, or product destruction tied to obsolete devices seems complete once the equipment leaves the building. From an audit standpoint, that's only halfway done. The test is whether the documentation can stand alone years later.

What auditors usually need to see

For IT asset disposition, the most defensible file usually connects several records:

- Asset identity: serial number, tag number, model, location, or other unique identifier.

- Disposition trigger: refresh cycle, lease return, failure, consolidation, office move, or decommissioning.

- Custody trail: who released the equipment, who transported it, and who received it.

- Data handling evidence: proof that drives, media, or embedded storage were sanitized or destroyed.

- Management review: clear indication that someone checked and accepted the record.

A missing piece doesn't always mean misconduct. It often means the organization can't prove that its process worked as designed.

Practical rule: If a third party can't reconstruct the transaction from the file alone, the file isn't finished.

Why this now sits with operations too

Audit documentation used to be treated as a finance issue. That no longer fits reality. Device retirement crosses finance, information security, legal, procurement, ESG reporting, and operations. Medical equipment disposal raises one set of handling questions. Data center decommissioning raises another. Social enterprise recycling and corporate donation programs add another layer because donated devices still need documented control and decision records.

For companies managing sustainable recycling and IT equipment disposal at scale, audit preparedness has to be built into the workflow at the moment equipment is collected, processed, and approved. Reconstructing it later is slower, weaker, and much harder to defend.

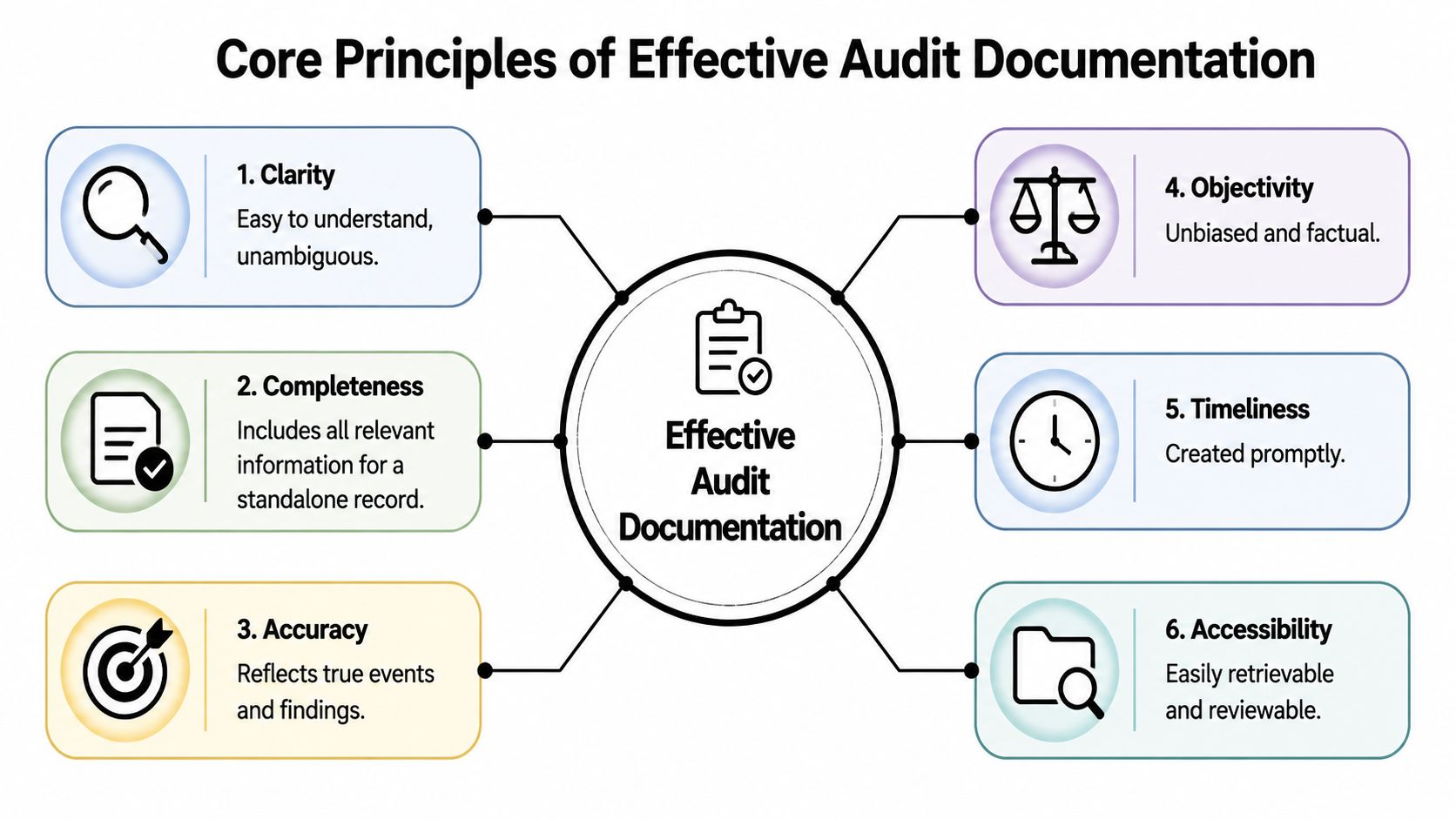

Core Principles of Effective Audit Documentation

The best documentation does three things at once. It proves the work happened, it supports the conclusion, and it allows another qualified person to review what was done without relying on memory or hallway explanations. Those principles sound basic, but they're where most files either become durable or fall apart.

According to AU-C Section 230 paragraph .08, audit documentation must capture the “nature, timing, and extent of the procedures performed”. That matters because vague records don't show enough. “Drives destroyed” is not the same as documenting what was handled, when it was handled, and how broadly the procedure was applied.

What good documentation looks like in practice

A strong file is usually built around six habits.

- Clarity: the record uses plain labels, readable descriptions, and direct links between assets, actions, and outcomes.

- Completeness: the file includes the supporting records needed to understand what happened from start to finish.

- Accuracy: asset IDs, dates, reviewers, and results match the underlying systems and physical reality.

- Objectivity: the record notes facts, not assumptions.

- Timeliness: documents are created close to the event, before details drift.

- Accessibility: the team can retrieve the file quickly during an audit, investigation, or customer inquiry.

If your organization manages electronics recycling through multiple locations, these principles become even more important. Central policy won't help much if site-level records are inconsistent or impossible to retrieve.

Why standalone records matter

A common failure is overreliance on institutional memory. Someone says, “That batch was part of the spring cleanout,” or “the vendor always destroys drives on pickup.” Auditors won't accept routine as evidence. They need the record tied to the specific transaction.

That's also why asset tracking systems are so important. A documented process supported by a retrievable system is much easier to defend than a collection of disconnected spreadsheets. Teams building stronger controls should look at how asset tracking systems support traceability from collection through final disposition.

Good documentation should answer four questions without a meeting: What was done, who did it, when it happened, and why the conclusion makes sense.

Understanding Key Regulatory Frameworks

Different organizations face different documentation frameworks, and confusion often starts when teams assume one standard covers every situation. It doesn't. The rulebook depends on whether you're dealing with a public company audit, a private-company audit, or a management-system audit tied to operational controls.

PCAOB and public company expectations

For public company audits in the United States, the Public Company Accounting Oversight Board sets the documentation standard. In practical terms, PCAOB rules push for a file that is traceable, reviewable, and explicit about who performed and reviewed the work. This framework tends to be especially relevant when IT asset disposition affects financial reporting, internal control testing, cybersecurity governance, or legal exposure from secure data destruction failures.

AICPA and private company or nonprofit environments

Private companies and nonprofits often look to the AICPA framework. A major turning point came in 2002, when SAS No. 96 required auditors to document significant findings or issues and the basis for final conclusions. That shift matters beyond accounting. It established the expectation that important judgments can't live only in email threads or verbal explanations.

For IT and operations teams, this translates into a simple lesson. If an equipment retirement involved an unusual decision, such as partial reuse, donation-based recycling, or exception handling for damaged media, the reasoning should be preserved in the file.

ISO and operational audit evidence

The ISO world often applies when your organization is audited against management systems such as information security, quality, or environmental controls. That context can directly touch electronics recycling, medical equipment disposal, laboratory equipment disposal, and broader sustainable recycling programs because the audit focus is often on process conformity, sampling, and retained evidence.

Teams that work across jurisdictions sometimes benefit from plain-English references on how standards are interpreted in practice. A concise example is Safety Space's guide to auditing standards, which helps frame how documented evidence, independence, and audit quality are discussed outside the U.S. regulatory lens.

How to decide which framework matters most

Use the framework that matches the engagement, then build operational records so they can support more than one review. That usually means:

| Organization context | Primary documentation lens |

|---|---|

| Public company external audit | PCAOB |

| Private company or nonprofit financial statement audit | AICPA |

| Management system audit such as information security or environmental controls | ISO |

A smart documentation process doesn't force the business to rebuild evidence for each new audit type. It creates records once, correctly, and stores them so multiple stakeholders can rely on them.

What Exactly Must Be Documented A Checklist

Audit files fail for predictable reasons. They don't identify the population tested. They don't show who reviewed the work. They preserve the conclusion but not the basis for it. The fix is not more paperwork for its own sake. The fix is a file structure that captures the minimum record needed to prove the work.

Under PCAOB AS 1215, audit documentation must show that the work was performed, identify who performed it, who reviewed it, and the date of review, with enough detail to explain the purpose, source, and conclusions reached. That language is strict for a reason. Accountability disappears when names, dates, and purpose are left implied.

The essential contents of a defensible file

For most audit-related workflows, the file should include:

- Scope records: what process, location, asset group, or disposal event was under review.

- Planning documents: criteria, objectives, risk focus, and any sampling approach used.

- Procedure records: the actual steps performed, not just the final outcome.

- Evidence references: source systems, uploaded files, photographs if used, contracts if relevant, and supporting confirmations.

- Results and conclusions: what the team found and what conclusion followed.

- Review evidence: preparer, reviewer, and review date.

When companies run office cleanout or facility cleanout projects, these basics matter because disposal events tend to be fast-moving and decentralized. People assume someone else has the master file. Often, no one does.

Checklist for ITAD and disposal-related workpapers

Use this as a practical control list:

- Identify the asset population clearly. Include serial numbers or another unique asset identifier.

- Document the source of selection. Show how the batch was chosen or separated.

- Tie each procedure to a purpose. For example, verifying pickup, confirming destruction, or validating donation eligibility.

- Preserve the underlying evidence. Don't rely only on summary sheets.

- Record signoffs properly. Preparer and reviewer details must be visible.

- Explain exceptions. If a device was missing, damaged, or redirected, document what happened and why.

Standardized templates help here, but only if they're practical enough for busy teams to use. Even process tools from outside audit can reinforce discipline. A good example is this guide to 5S for marketing teams, which shows how checklist structure and visual order reduce omissions in repeatable workflows.

For destruction events specifically, teams often benefit from using a consistent certificate format that forces key fields to be captured every time. A structured destruction certificate template can reduce the risk of missing asset IDs, dates, and authorization details.

Field note: The strongest files don't just show the outcome. They preserve the path that led to it.

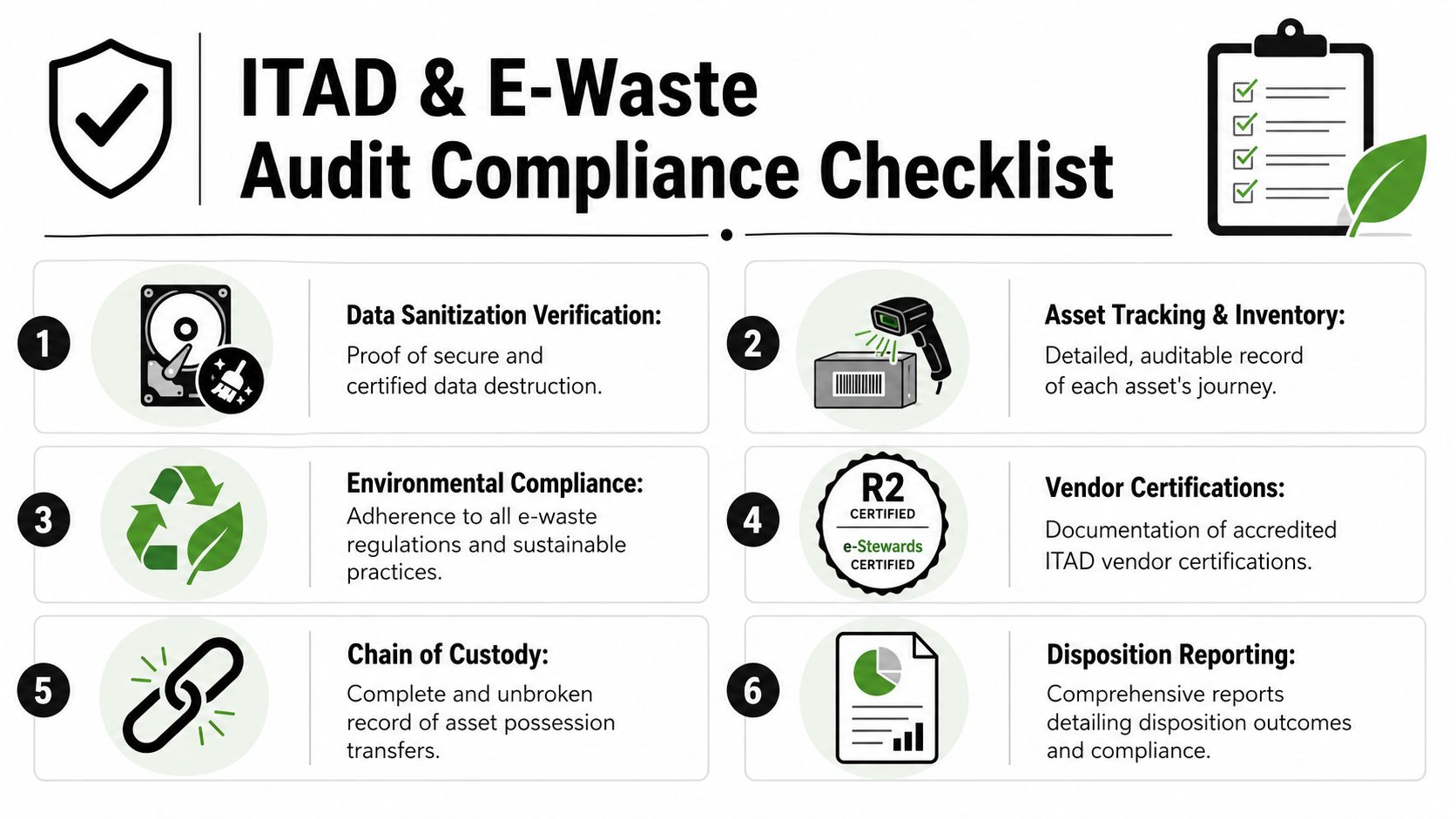

Applying Requirements to IT Asset Disposition and E-Waste

IT asset disposition is where abstract documentation rules become physical. Servers leave racks. Laptops leave desks. Drives move into bins for shredding. A recycler receives pallets. If those steps aren't documented tightly, the company can't prove secure handling, responsible recycling, or proper release of assets from control.

For ITAD, the audit file should connect the asset inventory, the custody trail, the data handling record, and the final disposition outcome. That applies whether the organization is managing computer recycling, secure data destruction, donation-based recycling, product destruction, or a blended program that includes resale, redeployment, and recycling.

The records that matter most in ITAD

For a disposal event, I look for a file that includes these core elements:

- Serialized asset list: what equipment was in scope.

- Pickup or transfer record: who released the assets and when.

- Chain of custody documentation: every transfer point from internal control to downstream handling.

- Data destruction evidence: a certificate or equivalent proof tied to the actual assets or media.

- Disposition report: whether the equipment was recycled, destroyed, refurbished, or directed into corporate donation programs.

- Exception log: missing drives, unreadable labels, broken devices, or split handling decisions.

A chain of custody file is especially important because the asset's risk doesn't end when it leaves your premises. It only ends when the documentation shows uninterrupted control and final disposition. Teams formalizing this process should build around chain of custody documentation rather than treating transfer forms as optional.

Sampling and batch verification

According to ISO 19011:2018 Clause 6.3.4, audit documentation must retain evidence of conformity, including the rationale for sampling methodology and clear identification of sample sizes. In ITAD terms, that matters when a company verifies a batch of destroyed hard drives or reviews only part of a decommissioned environment.

If you sample a subset of drives from a larger destruction event, document why that sample was chosen and what deviations were observed. “Spot checked a few units” is not enough. Auditors need to understand the logic of the test.

What works and what fails

What works is boring, repeatable discipline. Barcoded assets. Matched serial lists. Consistent release forms. Certificates linked back to the batch. Reviewed exception notes.

What fails is fragmented evidence. A pickup confirmation without serial numbers. A recycling certificate that doesn't specify what was processed. A donation record with no approval trail. For e-waste and ITAD, documentation quality is often the difference between a controlled disposition program and a hopeful one.

Record Retention Timelines and Security Protocols

Retention is where many organizations discover they've confused operational convenience with compliance. A file that was complete at the time of disposal is still useless if it was deleted early, stored in a mailbox no one can access, or changed without a defensible audit trail.

One major shift is the PCAOB's shorter documentation completion window. A change under AS 1000 reduces the completion period from 45 days to 14 days after the audit report for audits ending after December 15, 2024, with later timing for smaller firms. For business leaders, the practical point is simple. Supporting records have to be organized earlier, reviewed faster, and locked down with less room for cleanup after the fact.

Audit documentation retention period comparison

| Standard/Body | Minimum Retention Period |

|---|---|

| PCAOB | Qualitatively longer-term retention is required under PCAOB rules |

| AICPA | Qualitatively shorter than PCAOB in many organizations' policies |

The key point for operating teams is not to memorize a chart. It's to align your corporate policy with the strictest applicable requirement and make sure disposal records sit inside that policy, not outside it in ad hoc vendor folders or local drives.

Security controls for retained records

Strong retention without strong security still leaves the company exposed. The file should be protected against unauthorized access, silent revision, and accidental loss.

Use controls such as:

- Access restriction: limit who can view, edit, approve, and export records.

- Version control: preserve a visible history of additions and changes.

- Immutable storage where appropriate: especially for final signed records and destruction evidence.

- Central indexing: make retrieval fast enough for real audit response timelines.

- Vendor record integration: don't let essential evidence remain only in a third-party portal.

A written policy helps, but an operational retention framework is what keeps the record usable over time. Teams looking to tighten this area should map their procedures against formal record retention policies and confirm that ITAD, electronics recycling, and data destruction records are explicitly included.

Preserve documentation like evidence, not like general office files. The storage model should assume future scrutiny.

Common Pitfalls and Best Practices for Audit Readiness

Most audit documentation failures are ordinary. No one intended to create risk. The team moved quickly, trusted a vendor, skipped the final review, or assumed the certificate would be enough by itself. Then an auditor asks a precise question and the file can't answer it.

A critical example comes from PCAOB AS 1215, which requires documentation not only of evidence that supports the conclusion, but also information that “inconsistent with or contradicts the auditor's final conclusions.” That principle matters in operations too. If an asset count doesn't reconcile, if one drive was missing from a destruction batch, or if labels were unreadable, the file should show the issue and the resolution. Hiding the exception weakens the file more than recording it.

Pitfalls that repeatedly undermine audits

Some failures show up again and again:

- Incomplete linkage: the destruction certificate doesn't tie back to the exact asset population.

- Missing reviewer evidence: work was done, but no one formally reviewed or approved it.

- Exception silence: contradictory facts were known but never documented.

- Overreliance on vendor summaries: the company retained a high-level report but not the underlying support.

- Late assembly: the file was built only after the audit request arrived.

These mistakes show up in laptop disposal, medical equipment disposal, and decommissioning work because the operational event gets all the attention while the final record gets treated as an afterthought.

Best practices that actually hold up

The most reliable improvements are procedural, not rhetorical.

- Standardize forms: use consistent intake, transfer, and disposition documents.

- Require reconciliation: compare inventory, pickup records, and final disposition outputs before closing the file.

- Capture exceptions openly: document what didn't align and how it was resolved.

- Run internal spot checks: review a sample of closed files before an external auditor does.

- Choose vendors with documentation maturity: not just processing capacity.

Vendor selection matters because weak downstream documentation becomes your problem in an audit. Procurement and IT teams should use documented vendor selection criteria that test for chain of custody discipline, reporting quality, and evidence retention.

A company is audit-ready when its records can survive personnel changes, system migrations, and hard questions. That standard is much higher than “we usually keep the paperwork.”

How Reworx Recycling Delivers Audit-Proof ITAD Documentation

When companies outsource electronics recycling or IT asset disposition, they shouldn't have to choose between operational convenience and defensible records. The right partner reduces workload by producing cleaner evidence, not by asking your team to reconstruct it later.

Reworx Recycling supports that model by aligning operational handling with the documentation businesses need for audit response, internal control reviews, and customer due diligence. For companies managing computer recycling, secure data destruction, office cleanout events, facility cleanout projects, or data center decommissioning, that means records tied to specific assets and specific disposition outcomes.

What that solves for business teams

A strong ITAD partner should help you answer the questions auditors ask:

- What assets were released?

- Who handled them?

- What happened to the data?

- What was reused, donated, or recycled?

- Where is the final record?

That's especially important for organizations that care about donation-based recycling, social enterprise recycling, and community impact in addition to compliance. Responsible disposition isn't only about removing risk. It's also about supporting digital inclusion, workforce development, and sustainable recycling in a way the business can document credibly.

The practical advantage is straightforward. When serialized tracking, chain of custody, and final certificates are built into the service model, audit preparation becomes retrieval work instead of reconstruction work.

Frequently Asked Questions About Audit Documentation

Who owns audit documentation for disposed IT assets

Ownership is usually shared, but accountability shouldn't be vague. Finance may care about asset retirement. IT may own the equipment list. Security may own sanitization requirements. Procurement may manage the vendor. Someone still needs to own the final file and confirm it's complete.

Is a certificate of destruction enough by itself

Usually not. A certificate is important, but it's only one piece of the record. Auditors often need to see how the certificate connects to the asset list, the transfer record, and any exceptions.

Should donated equipment be documented differently from recycled equipment

Yes. The core controls are similar, but donation flows need clear approval, eligibility, asset condition assessment, and evidence of final transfer. If your company uses corporate donation programs, the file should still show control over data handling and final disposition.

What if part of the record lives with a vendor

That's common, but it's risky if your team can't retrieve it quickly. Pull critical records into your own retention environment rather than relying exclusively on portal access or vendor staff availability.

How often should teams test their documentation process

Often enough that problems surface before an auditor finds them. Internal reviews after office moves, refresh cycles, or decommissioning events are especially useful because those projects generate the most record complexity.

If your organization needs a more defensible approach to electronics recycling, IT equipment disposal, secure data destruction, or donation-based recycling, Reworx Recycling can help you build a cleaner documentation trail while supporting community impact through technology donations, digital inclusion, and workforce development. Businesses can explore pickup options, donate old equipment, or start a conversation about a compliant ITAD partnership that holds up under audit.